import yfinance as yf

import pandas as pd

import numpy as np

import matplotlib

matplotlib.use("Agg")

import matplotlib.pyplot as plt

import seaborn as sns

import os

# Optional (für p-value / regression)

try:

from scipy import stats

HAS_SCIPY = True

except Exception:

HAS_SCIPY = False

TICKERS = ["QQQ", "SPY", "IWM", "DIA", "^GDAXI"]

START = "1990-01-01"

END = None

N_JAN = 5

BOOTSTRAP_ITERS = 10000

SEED = 42

def plot_jan_effect(df, ticker, n_jan, save_dir="plots"):

os.makedirs(save_dir, exist_ok=True)

sns.set_style("whitegrid")

# 1) Scatter

fig = plt.figure(figsize=(8, 6))

colors = df["JanPos"].map({True: "green", False: "red"})

plt.scatter(df["JanRet"]*100, df["YearRet"]*100, c=colors, alpha=0.7)

plt.axhline(0, linewidth=1)

plt.axvline(0, linewidth=1)

plt.xlabel(f"Return first {n_jan} trading days of January (%)")

plt.ylabel("Full year return (%)")

plt.title(f"{ticker} – January Effect Scatter")

plt.tight_layout()

fig.savefig(os.path.join(save_dir, f"{ticker}_01_scatter.png"), dpi=160)

plt.close(fig)

# 2) Boxplot

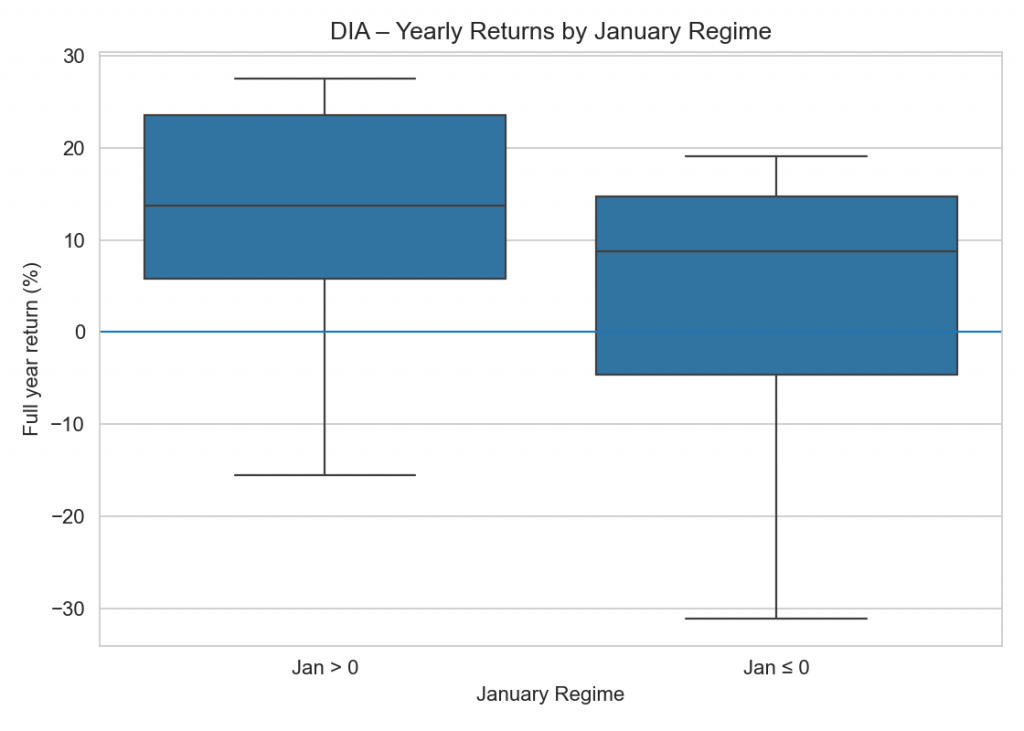

fig = plt.figure(figsize=(7, 5))

sns.boxplot(

x=df["JanPos"].map({True: "Jan > 0", False: "Jan ≤ 0"}),

y=df["YearRet"] * 100

)

plt.axhline(0, linewidth=1)

plt.xlabel("January Regime")

plt.ylabel("Full year return (%)")

plt.title(f"{ticker} – Yearly Returns by January Regime")

plt.tight_layout()

fig.savefig(os.path.join(save_dir, f"{ticker}_02_boxplot.png"), dpi=160)

plt.close(fig)

# 3) Equity-style

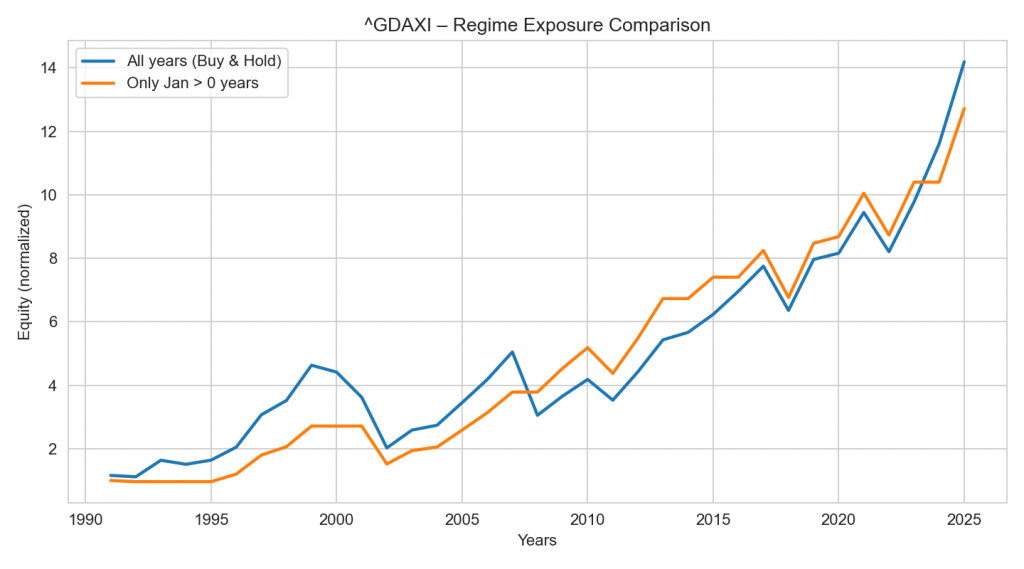

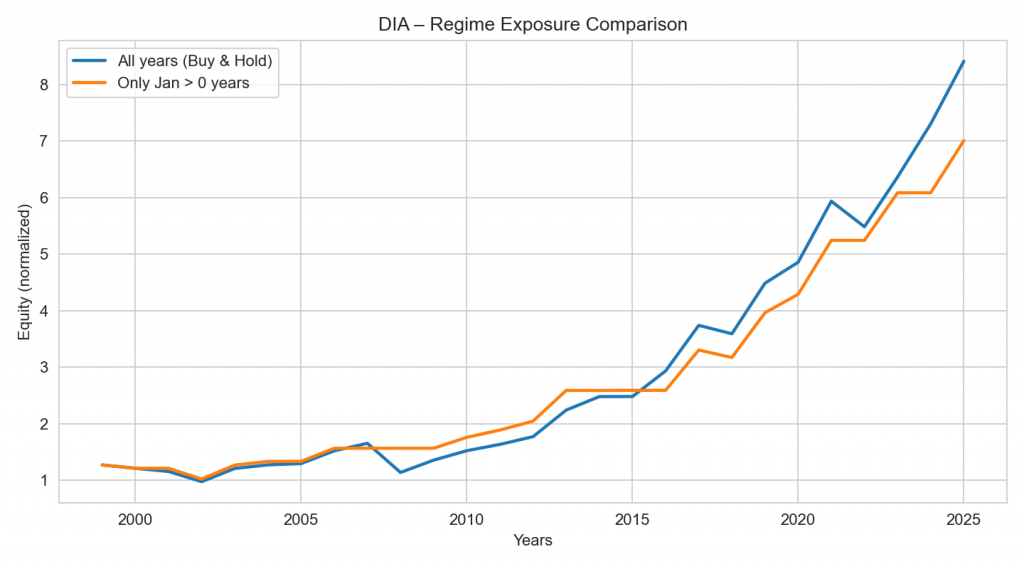

equity_all = (1 + df["YearRet"]).cumprod()

equity_jan_pos = (1 + df["YearRet"].where(df["JanPos"], 0)).cumprod()

fig = plt.figure(figsize=(9, 5))

plt.plot(df.index, equity_all.values, linewidth=2, label="All years (Buy & Hold)")

plt.plot(df.index, equity_jan_pos.values, linewidth=2, label="Only Jan > 0 years")

plt.legend()

plt.title(f"{ticker} – Regime Exposure Comparison")

plt.ylabel("Equity (normalized)")

plt.xlabel("Years")

plt.tight_layout()

fig.savefig(os.path.join(save_dir, f"{ticker}_03_equity.png"), dpi=160)

plt.close(fig)

def download_close_series(ticker: str) -> pd.Series:

df = yf.download(ticker, start=START, end=END, auto_adjust=True, progress=False)

if df is None or df.empty:

raise ValueError(f"No data returned for {ticker}.")

# yfinance returns columns like Open/High/Low/Close/Volume

# Ensure Close is a Series (not a DataFrame)

close = df["Close"]

if isinstance(close, pd.DataFrame):

# If something weird happens, take first column

close = close.iloc[:, 0]

close = close.dropna()

close.name = "Close"

return close

def compute_year_table(close: pd.Series, n: int) -> pd.DataFrame:

s = close.dropna().copy()

s = s.sort_index()

years = sorted(s.index.year.unique())

rows = []

for y in years:

s_y = s[s.index.year == y]

if s_y.empty:

continue

# January subset

s_jan = s_y[s_y.index.month == 1]

if len(s_jan) < n:

continue

jan_first_date = s_jan.index[0] # Timestamp

jan_n_date = s_jan.index[n - 1] # Timestamp

# previous trading day close before first January trading day

# robust approach: locate position via integer location

pos_first = s.index.get_loc(jan_first_date)

if isinstance(pos_first, slice) or isinstance(pos_first, np.ndarray):

# extremely rare, but handle duplicates defensively

pos_first = pos_first.start if isinstance(pos_first, slice) else int(pos_first[0])

if pos_first == 0:

continue

prev_close = float(s.iloc[pos_first - 1])

jan_n_close = float(s.loc[jan_n_date])

jan_ret = jan_n_close / prev_close - 1.0

# full-year return: first close of year to last close of year

year_ret = float(s_y.iloc[-1] / s_y.iloc[0] - 1.0)

rows.append({

"Year": y,

"JanRet": jan_ret,

"YearRet": year_ret,

"JanPos": jan_ret > 0,

"YearPos": year_ret > 0

})

df = pd.DataFrame(rows)

if df.empty:

raise ValueError("No valid yearly rows found. Check start date / data.")

return df.set_index("Year")

def summarize(df: pd.DataFrame, bootstrap_iters: int = 10000, seed: int = 42) -> dict:

pos = df[df["JanPos"]]

neg = df[~df["JanPos"]]

out = {}

out["Years"] = len(df)

out["HitRate_Pos"] = float(pos["YearPos"].mean()) if len(pos) else np.nan

out["HitRate_Neg"] = float(neg["YearPos"].mean()) if len(neg) else np.nan

out["MeanYear_Pos"] = float(pos["YearRet"].mean()) if len(pos) else np.nan

out["MeanYear_Neg"] = float(neg["YearRet"].mean()) if len(neg) else np.nan

out["Diff_PosMinusNeg"] = out["MeanYear_Pos"] - out["MeanYear_Neg"]

out["Corr_Jan_Year"] = float(df["JanRet"].corr(df["YearRet"]))

# Welch t-test (optional)

if HAS_SCIPY and len(pos) >= 2 and len(neg) >= 2:

t, p = stats.ttest_ind(pos["YearRet"], neg["YearRet"], equal_var=False, nan_policy="omit")

out["Welch_pvalue"] = float(p)

else:

out["Welch_pvalue"] = np.nan

# Bootstrap CI for diff of means

if len(pos) and len(neg):

rng = np.random.default_rng(seed)

pos_vals = pos["YearRet"].to_numpy()

neg_vals = neg["YearRet"].to_numpy()

diffs = np.empty(bootstrap_iters, dtype=float)

for i in range(bootstrap_iters):

diffs[i] = rng.choice(pos_vals, size=len(pos_vals), replace=True).mean() - \

rng.choice(neg_vals, size=len(neg_vals), replace=True).mean()

out["CI_2.5"] = float(np.percentile(diffs, 2.5))

out["CI_97.5"] = float(np.percentile(diffs, 97.5))

else:

out["CI_2.5"] = np.nan

out["CI_97.5"] = np.nan

return out

def pct(x):

return "n/a" if pd.isna(x) else f"{100*x:,.2f}%"

def run():

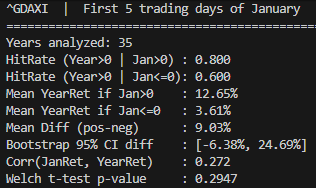

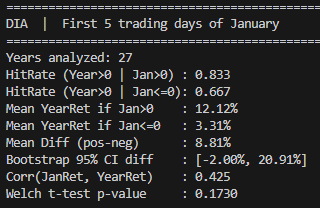

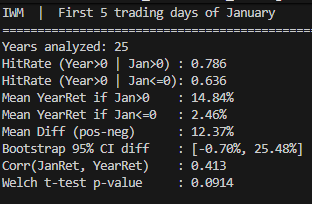

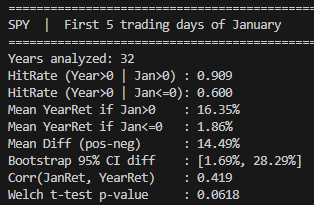

print(f"Settings: N_JAN={N_JAN}, START={START}, tickers={TICKERS}")

for ticker in TICKERS:

print("\n" + "=" * 90)

print(f"{ticker} | First {N_JAN} trading days of January")

print("=" * 90)

close = download_close_series(ticker)

year_table = compute_year_table(close, N_JAN)

stats_out = summarize(year_table, BOOTSTRAP_ITERS, SEED)

print(f"Years analyzed: {stats_out['Years']}")

print(f"HitRate (Year>0 | Jan>0) : {stats_out['HitRate_Pos']:.3f}")

print(f"HitRate (Year>0 | Jan<=0): {stats_out['HitRate_Neg']:.3f}")

print(f"Mean YearRet if Jan>0 : {pct(stats_out['MeanYear_Pos'])}")

print(f"Mean YearRet if Jan<=0 : {pct(stats_out['MeanYear_Neg'])}")

print(f"Mean Diff (pos-neg) : {pct(stats_out['Diff_PosMinusNeg'])}")

print(f"Bootstrap 95% CI diff : [{pct(stats_out['CI_2.5'])}, {pct(stats_out['CI_97.5'])}]")

print(f"Corr(JanRet, YearRet) : {stats_out['Corr_Jan_Year']:.3f}")

if not pd.isna(stats_out["Welch_pvalue"]):

print(f"Welch t-test p-value : {stats_out['Welch_pvalue']:.4f}")

print("\nLast 8 years:")

tail = year_table.tail(8).copy()

tail["JanRet"] = tail["JanRet"].map(pct)

tail["YearRet"] = tail["YearRet"].map(pct)

print(tail[["JanRet", "YearRet", "JanPos", "YearPos"]].to_string())

# 🔥 HIER die Plots

plot_jan_effect(year_table, ticker, N_JAN)

if __name__ == "__main__":

run()